AmBank’s Debt Consolidation Plan (AmMoneyLine/AmMoneyLine-i) is a personal financing product designed to pay your existing creditors directly. AmBank markets this as helping avoid double-counting existing commitments in your DSR assessment – which can solve the catch-22 that gets many Malaysians rejected elsewhere.

If your debt-to-income ratio is borderline and other banks keep turning you away, AmBank might be your way out.

Key Takeaways:

- AmBank pays your creditors directly (primarily direct payoff; any excess may be disbursed to your account)

- Marketed as avoiding DSR double-counting of existing debts

- Rates: 4.88% – 11.99% flat (8.78% – 21.58% EIR) per official published range

- Max amount: Up to RM150,000 (subject to credit assessment)

- Max tenure: 7 years

- Best for: High DSR cases, private sector, self-employed

Table of Contents

Quick Overview

| Feature | Details |

|---|---|

| Product Name | AmMoneyLine / AmMoneyLine-i |

| Interest Rate | 4.88% – 11.99% flat (EIR: 8.78% – 21.58%) |

| Financing Amount | RM2,000 – RM150,000 |

| Tenure | Up to 7 years (84 months) |

| Min Income | ~RM3,000/month (salaried), RM5,000/month (self-employed)* |

| Age | 21 – 60 years |

| Approval Time | Within 72 hours (with complete documents, per AmBank) |

| Key Feature | Direct payoff to creditors – no DSR double-count |

Industry practice: Most banks offer personal loan tenures up to 10 years. AmBank offers up to 7 years for this product.

Rates verified against AmBank PDS (effective 22 September 2025). Final rate, amount, and tenure subject to credit assessment. Always check the latest PDS and get pre-approval before committing.

What Is AmBank’s Debt Consolidation Plan?

AmBank’s Debt Consolidation Plan is a personal financing facility under the AmMoneyLine product line. Unlike standard personal loans where you receive cash and pay creditors yourself, AmBank settles your debts directly with your existing lenders.

This matters because most loan rejections happen due to high Debt Service Ratio (DSR). When you apply for a regular consolidation loan, banks see your existing debts PLUS the new loan – pushing your DSR over the 60% threshold. AmBank’s direct payoff mechanism removes your old debts from the equation before calculating your new DSR.

The product comes in two versions:

- AmMoneyLine – Conventional (interest-based)

- AmMoneyLine-i – Islamic (Shariah-compliant, Commodity Murabahah)

Both versions have identical rates, eligibility, and fees. The Islamic option provides Shariah compliance and ibra’ (rebate) on early settlement.

Note: AmMoneyLine offers two programs: Cash Out (funds deposited to your account) and Debt Consolidation (direct creditor payoff). This review covers the Debt Consolidation program only.

Important distinction: AmMoneyLine is different from AmBank’s Personal Financing-i (PF-i), which offers lower rates (from 3.45% for govt/GLC employees) but disburses cash to you – not directly to creditors. If your DSR is healthy, PF-i may offer better rates. But if you need direct payoff to solve DSR issues, AmMoneyLine is the product.

For full product details, refer to AmBank’s official AmMoneyLine page and Product Disclosure Sheet.

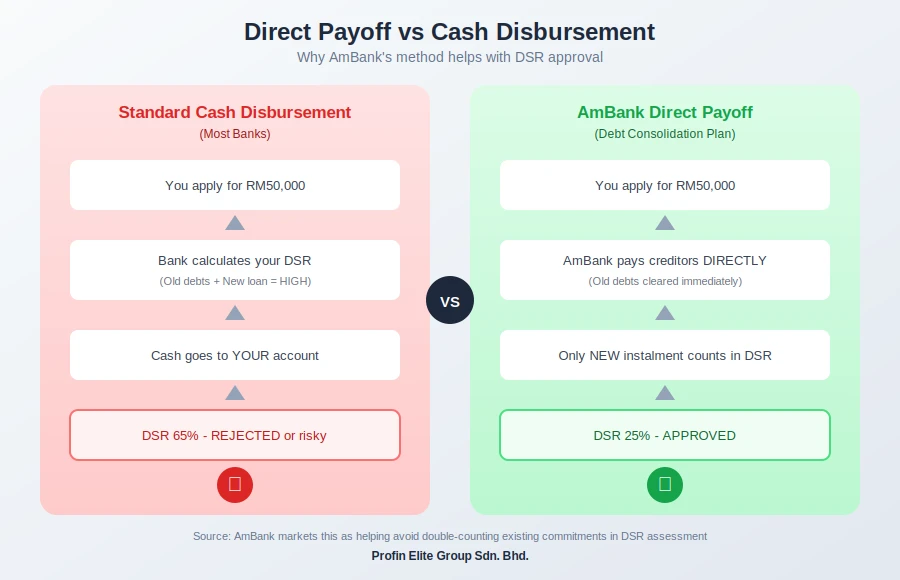

The Direct Payoff Advantage

This is AmBank’s killer feature. Here’s why it matters:

The problem with most debt consolidation:

You apply for RM80,000 to pay off existing debts. Bank checks your DSR. Your current loans are still showing as commitments. New loan adds more commitment. DSR shoots above 60%. Application rejected.

Catch-22.

How AmBank solves it:

With the Debt Consolidation Plan, AmBank pays your creditors directly – credit cards, personal loans, financing accounts. AmBank markets this as helping avoid double-counting your existing commitments when assessing affordability.

Result: Only your new AmBank instalment counts toward DSR. Old commitments are gone.

Example:

| Scenario | Without Direct Payoff | With AmBank Direct Payoff |

|---|---|---|

| Income | RM6,000 | RM6,000 |

| Existing commitments | RM2,400 | RM0 (paid off) |

| New loan instalment | RM1,500 | RM1,500 |

| Total commitments | RM3,900 | RM1,500 |

| DSR | 65% ✗ | 25% ✓ |

Same person. Same debt. Different outcome.

For a complete overview of debt consolidation options, see our Debt Consolidation Loan Malaysia guide.

Interest Rates

AmBank’s rates aren’t the lowest in the market. But if you can’t get approved elsewhere, rates become secondary.

Rate structure:

| Factor | Flat Rate | EIR |

|---|---|---|

| Official published range | 4.88% – 11.99% | 8.78% – 21.58% |

Lower promotional rates (from 4.88%) may apply to selected segments. Rates vary based on credit profile and financing amount.

Sample monthly payment calculation:

| Item | Amount |

|---|---|

| Loan amount | RM80,000 |

| Flat rate | 9.5% p.a. |

| Tenure | 5 years (60 months) |

| Total interest | RM80,000 x 9.5% x 5 = RM38,000 |

| Total repayment | RM118,000 |

| Monthly payment | RM1,967 |

Calculate your actual payment →

Early settlement rebate:

Settle early and you receive a rebate on unearned interest, calculated using the Rule of 78 formula. No penalty, but 1 month written notice required.

Note: A “Yearly Rebate Programme” existed, but per AmMoneyLine T&C (effective 22 Sep 2025), it is NOT applicable for customers who applied after 29 Feb 2024. Do not factor this rebate into your calculations for 2026 applications.

Realistic expectations:

Actual rates depend on your credit profile. The official range spans 4.88%-11.99% flat (8.78%-21.58% EIR). Not cheap compared to government servant products, but comparable to credit card balance transfer rates – and you get structured repayment.

Why not just do a balance transfer?

Balance transfers (0% for 6-12 months) work for small amounts you can pay off quickly. But if you have RM50,000+ in debt across multiple cards and loans, a structured consolidation loan with fixed payments is usually more sustainable.

Note on rate comparisons: Flat rates can be misleading – always compare using EIR (Effective Interest Rate) when evaluating options. The industry is moving toward EIR-only disclosures for transparency.

Islamic Option: AmMoneyLine-i

AmMoneyLine-i is the Shariah-compliant version using Commodity Murabahah (Tawarruq) concept.

Key features:

| Feature | Conventional | Islamic (Facility-i) |

|---|---|---|

| Structure | Interest-based | Profit rate (Tawarruq) |

| Stamp duty | 0.5% of loan amount | 0.5% of loan amount |

| Early settlement | No penalty (1 month notice) | Ibra’ (rebate) on unearned profit |

| Rates | 4.88% – 11.99% | 4.88% – 11.99% |

| Eligibility | Same | Same |

Why choose Islamic? Both products have identical rates and stamp duty. The main difference is Shariah compliance and the ibra’ mechanism – if you settle early, you receive a rebate on unearned profit. Choose based on your preference for Islamic financing principles.

For a detailed comparison of all Islamic debt consolidation options, see our Islamic Debt Consolidation Guide.

Who Can Apply

Quick Eligibility Check:

- ✓ Malaysian citizen or PR

- ✓ Age 21-60

- ✓ Income ~RM3,000+/month (salaried) or RM5,000+/month (self-employed, RM60k annual)

- ✓ Employed 6+ months with current employer

- ✓ Clean or recovering credit history

All eligibility subject to AmBank’s credit assessment.

Full eligibility details:

| Requirement | Details |

|---|---|

| Nationality | Malaysian citizen or PR working in Malaysia |

| Age | 21 – 60 years (at loan maturity) |

| Min Income (Salaried) | ~RM3,000/month* |

| Min Income (Self-employed) | RM5,000/month (RM60k annual)* |

| Employment | Min 6 months with current employer |

*Minimum income per bank practice; PDS states “subject to credit assessment.”

Age example: If you’re 56, maximum tenure is 4 years (to mature by age 60).

Who gets better rates:

- AmBank@Work partner company employees (highly selective)

- Existing AmBank customers

- Higher loan amounts (rates tier down)

Credit check: Check your credit standing via eCCRIS (free credit report) or CTOS credit report before applying. AmBank checks CCRIS/CTOS – poor credit history affects approval.

How Much Can You Borrow

| Limit | Amount |

|---|---|

| Maximum | Up to RM150,000 (subject to credit assessment) |

| Minimum | RM2,000 |

| Income cap | Up to 10x gross monthly income |

Which limit applies: The lower of either RM150,000 OR 10x income, subject to AmBank’s credit assessment.

Example:

- Income: RM8,000/month

- 10x income = RM80,000

- Maximum cap = RM150,000

- Your limit = RM80,000 (lower of the two, subject to approval)

⚠️ Pro Tip: Don’t Under-Apply

AmBank deducts the 0.5% stamp duty from your loan amount before disbursement to creditors.

The Trap: You owe RM20,000. You apply for RM20,000. AmBank deducts RM100 (stamp duty) and pays your creditor RM19,900. Your debt is not fully settled, the account remains open – and the DSR advantage fails.

The Fix: Always apply for slightly more than your exact debt total to cover the stamp duty deduction. For RM20,000 debt, apply for at least RM20,100.

What Debts Can You Consolidate

Yes:

- Credit cards (any bank)

- Personal loans from other banks

- Hire purchase (case by case)

- Other financing facilities

No:

- AmBank’s own loans (cannot consolidate AmBank debt with AmBank)

- Illegal money lenders

- PTPTN (possible but usually not practical)

Important: Funds go directly to your creditors. You choose which debts to settle during application.

Documents Required

Salaried employees (any ONE of these income proofs):

- Latest 1 month payslip + bank statement showing salary credit

- Latest 3 months payslips

- Latest 3 months EPF statement

- Latest EA Form (for MNC/GLC/PLC employees)

Self-employed:

- Business registration (SSM) – must be active for 2+ years

- Latest 6 months company bank statements

- MANDATORY: Latest Form B/BE with official tax payment receipt (bank statements alone are rarely accepted)

All applicants:

- MyKad (front and back)

- Statements of debts to be consolidated

Fees and Charges

| Fee | Amount |

|---|---|

| Processing Fee | None |

| Stamp Duty | 0.5% of loan amount (both conventional and Islamic) |

| Late Payment | 1% p.a. on overdue amount |

| Early Settlement | No penalty (1 month written notice required) |

Stamp duty example: RM100,000 loan = RM500 stamp duty

Note: The RM10 nominal stamp duty sometimes mentioned for Islamic financing applies to duplicate documents or certain letters of offer – not the primary facility agreement. Both AmMoneyLine and AmMoneyLine-i attract 0.5% stamp duty on the principal sum under the Stamp Act 1949.

Pros and Cons

| Pros | Cons |

|---|---|

| Direct payoff – no DSR double-count | Higher rates than govt servant products (vs 2-3%) |

| Approval within 72 hours (with complete docs) | Max 7-year tenure (some banks offer up to 10) |

| Online application via AmOnline | Age cap at 60 (vs 70 at Bank Rakyat) |

| Early settlement rebate (Rule of 78 formula) | Rates not as competitive for low-risk profiles |

| Both conventional and Islamic options | Cannot consolidate AmBank’s own loans |

| No processing fee | |

| Accepts self-employed and commission earners | |

| Islamic option: Ibra’ rebate on early settlement |

Who Should Apply

Best fit:

- DSR above 50% – direct payoff solves the approval problem

- Private sector employees with multiple credit card debts

- Self-employed or commission earners (few banks accept these)

- Anyone rejected elsewhere due to high DSR

Look elsewhere if:

- You’re a government servant (Bank Rakyat/RHB offer 2-3% rates)

- You need more than RM150,000

- You want tenure longer than 7 years

- Your DSR is already low (cheaper options exist)

- You qualify for AmBank’s Personal Financing-i (lower rates, but cash payout)

- You’re in severe financial distress (AKPK’s free debt management programme may be more appropriate)

AmBank Debt Consolidation vs Competitors (2026)

| Feature | AmBank | Bank Rakyat | RHB |

|---|---|---|---|

| Min Rate (2026) | 4.88% | 2.89% | 2.82% |

| Typical Rate | 9-11% | 5-7% (private) | 6-8% (private) |

| Max Amount | RM150,000 | RM200,000 | RM300,000 |

| Max Tenure | 7 years | 10 years | 10 years |

| Direct Payoff | ✓ Yes | ✗ No | ✗ No |

| Age Limit | 60 | 70 | 60 |

| Best For | High DSR cases | Govt servants | Higher amounts |

Rates approximate; verify latest PDS of each bank before applying.

When to choose AmBank: Your DSR is borderline. You’ve been rejected by other banks. You need the direct payoff mechanism to get approved.

When to choose Bank Rakyat: You’re a government servant wanting the lowest rates and longest tenure.

Read full Bank Rakyat review →

When to choose RHB: You need higher amounts (up to RM300,000) and have strong DSR.

How to Apply

Option 1: AmOnline (fastest for amounts under RM100k)

- Log into the AmOnline app

- Tap “More” → “Apply for More Services” → “Get Loan/Financing”

- Select “Debt Consolidation Plan”

- Crucial: When entering the amount, add RM200-RM500 buffer to cover stamp duty deductions

- Upload documents directly in the app

Note: Check the app for current maximum tenure available online.

Option 2: Branch Walk-In (best for complex cases)

Visit any AmBank branch. Bring your redemption statement (current balance) from your existing banks.

Ask the officer: “Please ensure the applied amount covers the 0.5% stamp duty so the net disbursement fully clears my old balance.”

Option 3: Through an advisor

If you have borderline DSR or complex income documents, work with a financial advisor (like Profin Elite) who can pre-calculate your eligibility before submitting.

Processing time: AmBank states approval can be within 72 hours with complete documentation. Actual timing depends on how quickly your existing banks provide settlement figures.

The Bottom Line

AmBank’s rates aren’t the cheapest. But that’s not the point.

The Debt Consolidation Plan exists for one reason: to help people who can’t get approved elsewhere. The direct payoff mechanism solves the DSR catch-22 that traps many Malaysians.

If your DSR is borderline, stop collecting rejections. AmBank’s direct payoff might be your way out.

Next Steps

Option 1: Calculate your potential savings using our debt consolidation calculator.

Option 2: Check your DSR to see where you stand.

Option 3: Compare all banks if your DSR is healthy.

Option 4: Talk to us – we’ll assess your situation and recommend the right approach.

Profin Elite is a financial advisory firm registered with SSM. We don’t lend money – we help you find the best terms from the right banks. Rates and terms verified against AmBank PDS (effective 22 Sep 2025); always confirm latest PDS and get pre-approval before committing.

FAQ

What is AmBank’s debt consolidation plan?

AmBank’s Debt Consolidation Plan (AmMoneyLine) is a personal financing product designed to pay your existing creditors directly. AmBank markets this as helping avoid DSR double-counting issues that cause rejections at other banks.

What is the main advantage of AmBank’s debt consolidation?

Direct payoff to creditors. AmBank uses the funds to settle your existing debts directly. AmBank markets this as helping avoid double-counting existing commitments in your DSR assessment – only the new AmBank instalment is counted.

How much interest does AmBank charge for debt consolidation?

4.88% to 11.99% flat per AmBank’s official published range (EIR 8.78%-21.58%). Lower promotional rates may apply to selected segments. Actual rate depends on your credit profile and financing amount.

Does AmBank pay off credit cards directly?

Yes. AmBank pays off your credit cards directly as part of their Debt Consolidation Plan. You can consolidate cards from any bank, including AmBank credit cards.

What if I have high DSR? Will I still get approved?

That’s exactly what AmBank’s direct payoff solves. Because they settle your old debts before calculating new DSR, many people with 50-70% DSR get approved.

How fast is AmBank’s approval?

AmBank states approval can be within 72 hours with complete documentation. Actual timing depends on document completeness and credit assessment.

Is there early settlement penalty?

No penalty, but you must give 1 month written notice before settling early. Islamic (Facility-i) customers receive ibra’ rebate on unearned profit.

Can self-employed apply?

Yes. Minimum income is RM5,000/month (RM60k annual) with business registration and 6 months bank statements. Rate is usually at the higher end of the 4.88%-11.99% range.

Is there an early settlement rebate?

Yes. If you settle early, you receive a rebate on unearned interest calculated using the Rule of 78 formula. No penalty applies, but you must give 1 month written notice. Note: A “Yearly Rebate Programme” existed, but per T&C (effective 22 Sep 2025), it is NOT applicable for applications after 29 Feb 2024.

What’s the difference between AmMoneyLine and AmBank Personal Financing-i?

AmMoneyLine (Debt Consolidation Plan) pays creditors directly and has rates from 4.88%. AmBank Personal Financing-i disburses cash to you and offers lower rates (from 3.45% for govt/GLC employees) but stricter eligibility. If your DSR is healthy, PF-i may be better. If you need direct payoff to solve DSR issues, AmMoneyLine is your option.

Is there a stamp duty difference between conventional and Islamic?

No. Both AmMoneyLine (conventional) and AmMoneyLine-i (Islamic) attract 0.5% stamp duty on the loan amount under the Stamp Act 1949. The RM10 nominal duty sometimes mentioned for Islamic financing applies only to certain duplicate documents, not the primary facility agreement.